Short Answer:

As a seasoned attorney with extensive experience in real estate transactions and business law, I understand the critical importance of a well-structured business lease agreement for the success of any company. A business lease serves as the foundation for your company’s physical presence and operations, setting the terms for occupancy, financial commitments, and the rights and responsibilities of both landlords and tenants. This guide aims to demystify the complexities of commercial leases, offering insights into effectively navigating and negotiating these agreements, as well as strategies for mitigating risks associated with property and vehicle leasing. With a focus on the essentials, from understanding different types of leases to mastering negotiation tactics, this article will empower you to manage your business lease with clarity, confidence, and a strategic approach, ensuring your company’s needs are met and your interests are protected.

Key Takeaways

- A business lease agreement is a complex, legally binding document between a landlord and a commercial tenant that outlines terms including rent, lease duration, and maintenance, without consumer protection laws applicable to residential leases.

- There are various types of commercial leases such as gross, net, percentage, and modified gross leases, each with distinct terms concerning rent and responsibility for property-related expenses.

- Successfully navigating a business lease agreement requires understanding key terms related to rent payments, maintenance responsibilities, insurance requirements, and compliance with accessibility standards, alongside effective negotiation skills for terms like tenant improvement allowances and early termination provisions.

Understanding Business Leases

Leasing commercial property can be an exciting step in your business journey. Signing a business lease agreement requires a deep understanding of its complexities. So, what exactly is a business lease? As per definition, a business lease, also known as a commercial lease, is a legally binding agreement between a landlord and a commercial tenant for the rental of commercial property. In the world of business leases, the two key players are the property owner (lessee) and the commercial tenant (lessor), which could be anything from a startup to a multinational corporation.

The process of a commercial lease agreement involves the landlord agreeing to lease commercial property to the tenant for a specified period, typically ranging from three to five years. Although it offers benefits like no upfront payment, tax breaks, lower maintenance costs, and a broad selection of options, possible downsides, such as variable rent and no equity growth, should not be overlooked.

Commercial Lease Agreements

A commercial lease agreement is the bedrock of your business’s relationship with its landlord. It is a legally binding document that specifies the rights and responsibilities of both parties. These agreements contain vital details such as:

- The property address

- Rent amount

- Lease duration

- Additional terms and conditions agreed upon by both parties.

The key components of a commercial lease agreement are:

- The parties to the lease

- Premises clause

- Use clause

- Rent payment

- Term clause

- Security deposit or letter of credit

Since these agreements are not subject to consumer protection laws like residential leases, businesses must ensure they comprehend their lease agreement thoroughly before signing.

Key Players in Business Leases

In the realm of business leases, there are multiple key players: the buyer, the seller, and an experienced commercial real estate broker. The roles and responsibilities of each player differ. For instance, the landlords in business leases are responsible for the maintenance of the building’s exterior, repair of structural and significant property components, and the upkeep of fixtures and fittings to ensure safety.

Moreover, leasing agents:

- Act as representatives for landlords

- Promote their properties and advocate for their interests during negotiations

- Strive to maintain positive relationships with landlords to ensure a diverse and appealing selection of rental properties.

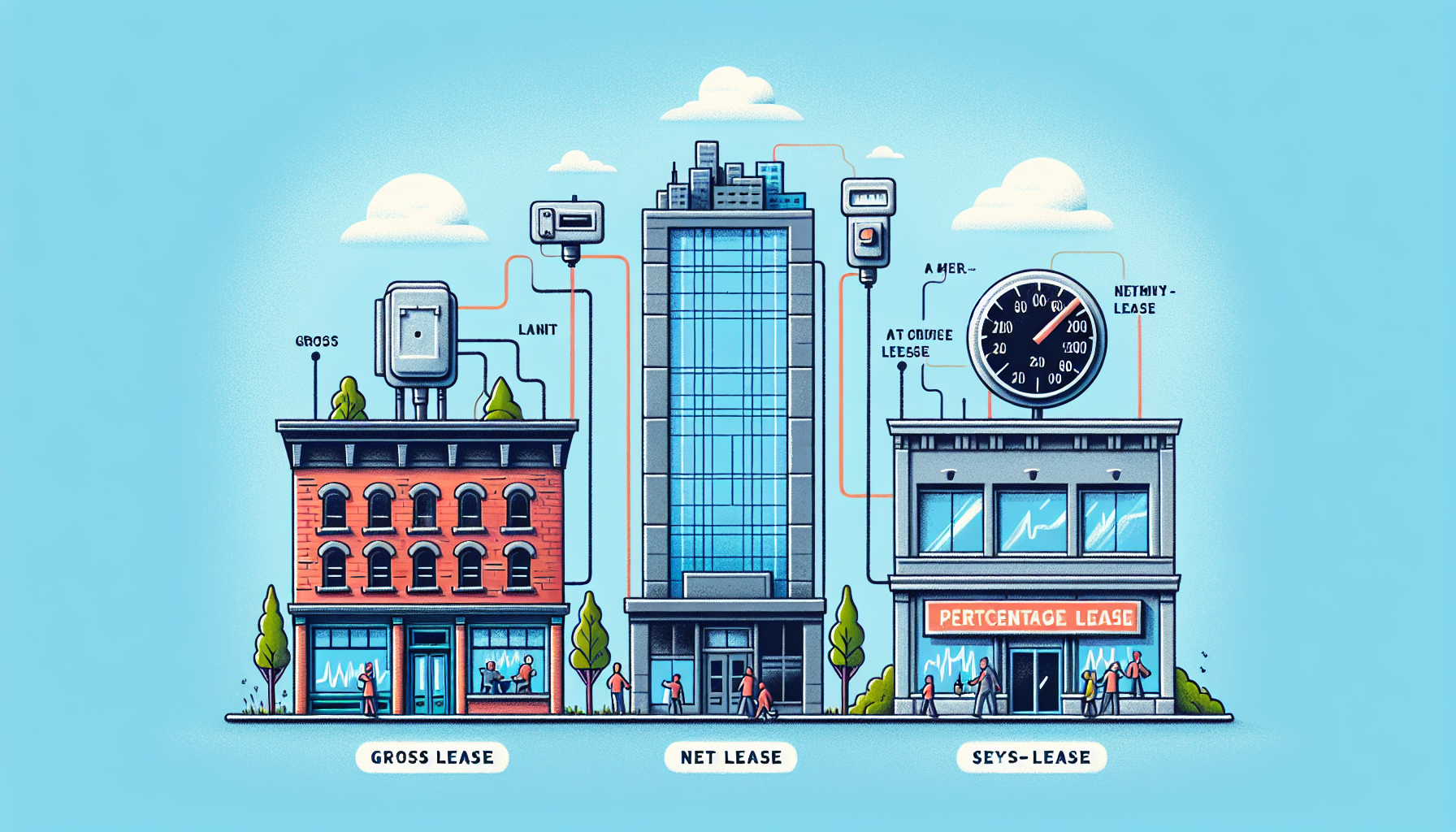

Types of Commercial Leases

Business lease agreements can take several forms, each with its own set of terms and conditions. Gaining insight into these various forms of commercial leases is key to selecting the best fit for your company. The most common types of commercial leases are:

- Gross lease

- Net lease

- Percentage lease

- Modified gross lease

A gross lease involves the tenant paying a fixed amount to use the property, while the landlord assumes responsibility for all property-related expenses. In contrast, a net lease requires the tenant to pay additional expenses such as property taxes, insurance premiums, and maintenance costs on top of their rental space.

A percentage lease involves the tenant paying a percentage of their revenues along with a base rent, a common arrangement in retail spaces located in shopping centers or malls. Lastly, a modified gross lease represents a blend of a gross lease and a net lease, where both the landlord and tenant shoulder some financial obligations for the property’s expenses.

Gross Lease

In a gross lease:

- The tenant pays a fixed amount that includes various expenses such as property taxes, utilities, building insurance, and other incidental charges.

- The landlord assumes the responsibility for all property-related costs.

- This lease type distinguishes itself from other leases, such as net leases, by its single flat fee that encompasses all property expenses.

- The landlord covers these costs.

Though this lease type provides stable rent payments and eases property management for landlords, it may lead to tenants paying higher rent compared to other leases, such as net leases, due to the landlord bearing property expenses.

Net Lease

A net lease involves the tenant assuming responsibility for supplementary expenses like property taxes, insurance premiums, and maintenance costs, in addition to the base rent. There are three categories of net leases:

- Single net lease (N): Tenant is responsible for property taxes.

- Double net lease (NN): Tenant is responsible for property taxes and insurance premiums.

- Triple net lease (NNN): Tenant is responsible for property taxes, insurance premiums, and maintenance costs.

Each category varies in the level of expenses the tenant is responsible for.

In a triple net lease (NNN), the tenant is responsible for paying:

- Rent

- Utilities

- Insurance

- Property taxes

- Maintenance costs

This lease type is advantageous for tenants seeking transparency in their monthly expenses, as it consolidates all property-related costs into a single set payment.

Percentage Lease

A percentage lease involves the tenant paying a base rent along with a percentage of their monthly sales that exceed a predetermined break-even threshold. This results in a rental arrangement that is somewhat contingent on the prosperity of the tenant’s business.

The percentage is commonly based on the sales revenue that surpasses a set threshold. Retail businesses and commercial establishments, particularly those located in shopping centers or areas with high foot traffic, commonly participate in percentage leases because of the sales volume-oriented nature of these businesses.

Modified Gross Lease

A modified gross lease is a lease structure that entails shared responsibility between the landlord and the tenant for paying a property’s operating expenses. This type of lease combines features of a gross lease, which includes all property expenses in the rent, and a triple net lease, where tenants are accountable for all property expenses.

Typical negotiable terms encompass:

- Base rent

- Expense allocation

- Maintenance responsibilities

- Lease term

- Renewal options

Commercial tenants can enjoy advantages such as reduced base rent, oversight of operating expenses, and minimized obligations for building upkeep with a modified gross lease.

From a landlord’s perspective, the advantages of a modified gross lease encompass the capability to distribute expenses with the tenant and the flexibility to transfer certain operating costs to the tenant.

Key Terms to Consider in a Business Lease Agreement

A thorough understanding of the key terms is indispensable for adeptly navigating a business lease agreement. These include:

- Rent and payment terms

- Maintenance and repair responsibilities

- Insurance requirements

- Accessibility and compliance provisions

The rent and payment terms typically encompass the monthly rent amount, known as the base rent, as well as provisions for potential rent increases on an annual basis or during lease renewal options, as stipulated in the rent escalation clause. Maintenance and repair responsibilities are typically divided between the landlord and the tenant, with the landlord generally responsible for the building’s exterior and the tenant responsible for interior repairs and routine maintenance.

Insurance requirements in a lease agreement often include general liability insurance and workers’ compensation insurance.

Lastly, accessibility and compliance terms in a lease agreement commonly include provisions to ensure accessibility for individuals with disabilities, in line with the Americans with Disabilities Act (ADA).

Rent and Payment Terms

In a business lease agreement, the standard rent and payment terms encompass the monthly rent amount, known as the base rent, as well as provisions for potential rent increases on an annual basis or during lease renewal options, as stipulated in the rent escalation clause. Supplementary expenses that could be encompassed in the rental fee for a commercial property include common area maintenance charges (CAM charges), operating expenses, utilities, electric, water, trash removal, security, landscaping, property taxes, repairs, administrative expenses, city permits, and insurance.

This complexity can make these agreements seem daunting, but understanding these terms is crucial to avoid unexpected costs and ensure a smooth business operation. It’s recommended to seek professional advice to ensure you fully understand these terms before signing a lease agreement.

Maintenance and Repairs

In a lease agreement, maintenance, and repair responsibilities are typically divided between the landlord and the tenant. The landlord is generally responsible for the building’s exterior and structural maintenance, while the tenant is responsible for interior repairs and routine maintenance.

If disputes or issues related to maintenance and repairs arise, the lease agreement should outline the procedure for resolution. This may involve specific dispute resolution mechanisms or guidelines for both parties to adhere to. It’s always advisable to negotiate these terms before signing the lease agreement to prevent potential disputes in the future.

Insurance Requirements

The typical insurance requirements outlined in a business lease agreement include general liability insurance and workers’ compensation insurance. The tenant is usually obligated to maintain liability insurance with a predetermined limit, such as $1,000,000 for each occurrence.

General liability insurance is crucial for landlords to safeguard themselves from potential liabilities stemming from the tenant’s business activities on the premises. On the other hand, personal property insurance is vital for tenants as it provides coverage against potential risks to business property, including theft, damage, or loss.

Accessibility and Compliance

Accessibility and compliance terms in a lease agreement often include provisions to ensure accessibility for individuals with disabilities, in line with the Americans with Disabilities Act (ADA). Both the tenant and the landlord have legal obligations to ensure ADA compliance, as specified in the lease. These obligations may include:

- Making accessibility modifications to the property

- Providing accessible parking spaces

- Installing ramps or elevators

- Ensuring accessible entrances and doorways

- Providing accessible restroom facilities

The lease should detail the party responsible for making these accessibility modifications and providing services. It is important for both parties to understand and comply with these obligations to ensure equal access for individuals with disabilities.

Failure to comply with ADA standards may lead to:

- hefty fines for the initial violation

- even heavier fines for subsequent violations

- legal ramifications

- potential harm to reputation

Therefore, it’s crucial to ensure your leased premises comply with these standards from the outset.

Leasing Options for Business Vehicles

When it comes to business vehicles, leasing often presents a more viable option than purchasing. There are several reasons why businesses may opt for leasing vehicles, including lower initial expenses and monthly payments, decreased maintenance responsibilities, and potential tax advantages.

The specific financial benefits of leasing a business vehicle include:

- Lower monthly payments and initial down payments

- Potential reduction in maintenance costs through included routine services

- Convenience of budgeting for vehicle expenses

In addition to these benefits, tax implications also play a crucial role in the decision-making process between leasing and purchasing a business vehicle.

Advantages of Leasing a Business Vehicle

Leasing a business vehicle can have a positive impact on cash flow by mitigating the need for a substantial upfront investment in purchasing a vehicle and instead opting for smaller monthly lease payments. Additionally, lease payments are categorized as operating expenses and may be eligible for tax deductions.

One of the key advantages of leasing a vehicle for business use relates to maintenance and repairs. The lease agreement will clearly outline the party responsible for covering these costs throughout the lease duration, often reducing out-of-pocket expenditures for business proprietors.

Furthermore, leasing facilitates the ability to change the vehicle at the conclusion of the lease term, offering the opportunity to stay current with new models and technology.

Tax Considerations

Understanding the tax implications is a vital aspect of leasing a business vehicle. If the leased car is used exclusively for business purposes, the entire cost of ownership and operation can be deducted. There are two methods for calculating car expenses: actual expenses or the standard mileage rate.

However, it’s important to note that both lease costs and the standard mileage rate cannot be deducted simultaneously. The individual must choose to either include the lease costs in their income or deduct the business portion of the lease costs.

Negotiating Your Business Lease Agreement

Negotiating a business lease agreement may seem daunting, particularly for novice lessees. Nevertheless, with adequate preparation and comprehension, you can negotiate lease terms that cater to your business requirements.

Certain aspects such as tenant improvement allowances, rent abatement, and early termination provisions can be key negotiation points in a lease agreement. Tenant improvement allowances, for example, refer to monetary provisions allocated by the landlord to offset a portion or all of the tenant’s expenses for customizing the leased space. Rent abatement is a contractual provision that grants tenants the option to temporarily suspend or decrease their rent obligations.

When discussing early termination provisions, it’s important to:

- Consider your rights and obligations

- Clearly communicate your intentions

- Explore various options and alternatives

- Approach the situation from the perspective of the landlord

- Thoroughly review the lease terms

- Seek professional assistance if necessary

- Potentially extend the lease duration

- Investigate possibilities such as lease buyouts or subleasing.

Tenant Improvement Allowances

Tenant improvement allowances (TIAs) are often a crucial part of lease negotiations. They refer to monetary provisions allocated by the landlord to offset a portion or all of the tenant’s expenses for customizing the leased space. The typical structure of tenant improvement allowances in commercial leases is a designated period of rent-free occupancy, often allocated within the initial year or distributed across the lease term.

However, negotiating these allowances can be challenging. It is essential for the involved parties to:

- Comprehend each other’s underlying interests

- Engage in the clarification and re-negotiation of terms

- Seek common ground

- Consistently maintain clear and respectful communication

This will help prevent any harm to the business relationship.

Rent Abatement and Free Rent Periods

Rent abatement or free rent periods can be a boon for tenants, especially startups and businesses with tight cash flow. These provisions entail a period during which the tenant is not obligated to pay rent, as mutually agreed upon by the landlord and the tenant.

However, landlords may hesitate to provide these concessions. It’s therefore important to negotiate these terms skillfully and present valid reasons for seeking such a concession, such as:

- the need for extensive renovations or improvements before the space is ready for use

- the need for additional time to secure financing or permits

- the need for flexibility in lease terms due to uncertain market conditions

By presenting these valid reasons, you increase your chances of successfully negotiating concessions with your landlord.

Early Termination and Subleasing

Early termination and subleasing options can provide flexibility for tenants. Early termination provisions allow the tenant to exit the lease before its official end date, usually by paying a penalty or meeting certain conditions. Subleasing allows the tenant to lease out either a part or the whole of the leased premises to another individual or business, offering financial flexibility and the ability to minimize financial loss in case of early termination.

When negotiating these provisions, it’s important to consider terms such as a written notice period, a termination charge or fee, and specified conditions for breaking the lease. These terms can provide a safety net and added flexibility for businesses.

Resolving Disputes in Business Leases

A range of issues, including non-payment and disagreements over lease terms, can lead to disputes in business leases. To ensure a smooth landlord-tenant relationship, it is crucial to know how to effectively resolve such disputes.

Non-payment issues in business leases can be resolved through mutual resolution and discussion between the parties involved. It is a common issue in commercial lease litigation. In the event of disagreements over business lease terms, it’s advisable to:

- Establish the grounds for the dispute

- Understand the lease agreement’s terms

- Engage in communication with the other party

- Focus on interests rather than positions

- Use objective criteria to resolve the issue.

In cases where resolution cannot be reached through negotiation, arbitration or mediation can be explored. Arbitration plays a crucial role as an alternative method for resolving disputes in business leases. It offers advantages such as confidentiality, expediency, and potential cost savings compared to conventional litigation.

Non-Payment Issues

Non-payment of rent is a common issue in commercial leases. This can be due to various reasons such as financial difficulties, disputes over service charges, or dissatisfaction with the landlord’s services. If a tenant fails to pay rent, the landlord can initiate eviction proceedings, which can be an efficient process once the notice period has expired.

However, commercial evictions afford fewer protections in comparison to residential evictions, and the penalties for early termination of a commercial lease can be severe, including:

- paying the remaining rent owed

- damaging the relationship with the landlord

- impacting the credit score

- potential legal claims

Thus, it’s important for tenants to ensure they understand their lease terms and seek professional advice if they’re facing difficulties in making payments.

Disagreements over Lease Terms

Disagreements over lease terms can arise due to a variety of reasons, such as misunderstandings, misinterpretations, or changes in circumstances. When such disputes arise, it’s important to follow a set of procedures.

The steps to resolve a dispute are as follows:

- Identify the issue and attempt to negotiate a resolution.

- If negotiation fails, consider mediation or arbitration.

- Consult a lawyer if necessary.

- Comply with the arbitration outcome to avoid further disputes.

- In extreme cases, legal action may be necessary to resolve the dispute.

Summary

Navigating a business lease agreement requires understanding of key terms, knowledge of different lease types, ability to negotiate favorable terms, and the skills to resolve potential disputes. This blog post has equipped you with the essential knowledge to confidently navigate your business lease agreement. We hope this guide helps you make informed decisions and navigate your business lease agreement with ease and confidence.

Frequently Asked Questions

What is a business lease?

A business lease is a contract between the owner of a property and a business, allowing the business to use the property for its operations in exchange for rent. It grants the business exclusive possession of the premises for a set period.

What is an example of leasing in business?

Leasing in business can involve the exchange of expensive physical goods, such as commercial and industrial fleet vehicles, production machines, forklifts, real estate, aircraft, and industry-specific machinery. It allows for the use of these assets without having to make a large capital expenditure.

What does lease agreement mean in business?

A lease agreement in business refers to a contract for renting office space or other business property from a landlord, specifically for business activities rather than housing. This allows businesses to secure a location for their operations.

What is a gross lease?

A gross lease means the tenant pays a fixed amount while the landlord covers property expenses, offering a simpler payment structure and less financial risk for the tenant.

What is a net lease?

A net lease requires the tenant to cover additional expenses such as property taxes, insurance, and maintenance, on top of the base rent. This type of lease transfers more financial responsibility to the tenant.