If you are a founder, a private equity buyout can look complicated from the outside because it is. But beneath the diagrams, commitment letters, and financing jargon is a simple question: what happens to your company, your control, and your upside after the deal closes? That is the part entrepreneurs should understand cold.

A buyout is not just a sale. It is a re-architecture of ownership. New money comes in, debt is layered onto the business, management incentives are reset, and the investor is already thinking about the next exit before the ink dries.

In this guide:

- What a buyout actually is

- Why entrepreneurs should care

- How to read the buyout structure graphic

- Private equity vs. strategic buyers vs. minority investors

- Common buyout structures founders see in the real world

- The documents and issues that really matter

- The founder mistakes that create regret later

- Companion topics worth writing next

- Use AI to pressure-test your deal

A buyout is three transactions happening at once

At a practical level, a private equity buyout combines three moving parts into a single closing. First, the buyer acquires the business. Second, the sponsor and often members of management put in equity. Third, lenders provide debt that helps finance the purchase price. Those pieces close together, not in separate silos, which is why buyouts feel dense and highly coordinated.

That distinction matters for founders. In a founder-led sale, you are not only negotiating value. You are negotiating a future capital structure, the company’s tolerance for leverage, the incentive plan for management, the level of post-closing control, and your own role after signing.

Why entrepreneurs should care even if they are not “doing private equity”

Many entrepreneurs assume private equity is relevant only when a mega-fund calls or an investment banker starts using the phrase auction process. In reality, the logic of buyouts shows up much earlier. It appears when a founder explores a partial exit, when management wants to roll equity, when a sponsor wants to make your company a platform, or when a larger portfolio company wants to acquire your business as an add-on.

If you understand the buyout playbook, you can ask better questions:

- How much of the purchase price is really cash at closing versus rollover equity or earnout-style upside?

- Will the post-closing business be able to carry the debt comfortably if growth slows down?

- Who controls the board, major decisions, hiring, and future acquisitions?

- Is your company being acquired as a standalone platform or folded into an existing roll-up?

- What has to go right for your retained equity to become meaningfully valuable?

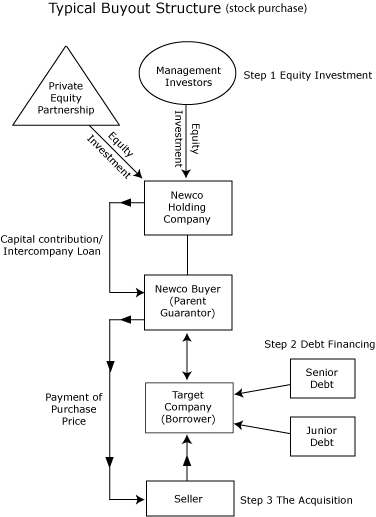

How to read the graphic without getting lost in the arrows

The diagram tells a simple story.

- Step 1: Equity comes in. The private equity sponsor and management investors put money into a newly formed holding company. Sometimes founders or executives roll some of their existing equity instead of taking all cash.

- Step 2: Debt gets layered onto the deal. Senior lenders, and sometimes junior or mezzanine lenders, finance part of the purchase price. This is what makes the deal a leveraged buyout when debt is a meaningful part of the stack.

- Step 3: The business is acquired. The buyer uses the sponsor’s equity plus the lenders’ money to pay the seller, and the target becomes part of the new ownership structure.

Private equity buyer, strategic buyer, or minority investor? These are very different conversations.

Private equity buyer

A sponsor is usually buying a company to grow it, professionalize it, and later exit it at a higher value. Management quality matters a lot because the investor is not usually absorbing your business into a giant operating machine on day one.

Strategic buyer

A strategic acquirer often cares most about fit. They may want your product, your customers, your team, or your market position because it strengthens an existing business they already run.

Minority investor

A minority investor is usually not buying control. They are buying influence, economics, and a negotiated set of protective rights. The company often remains founder-led.

Why founders get tripped up

These buyers can offer similar valuations while offering very different futures. The right comparison is not only price. It is price plus control, culture, leverage, liquidity, and your post-closing role.

Here is a plain-English example. Suppose a software founder has a $40 million offer from a strategic buyer and a $40 million offer from a private equity platform investor. Those two offers may feel equal, but they are not. The strategic buyer may want full integration and limited autonomy. The sponsor may want the founder to stay, roll equity, pursue add-on acquisitions, and grow toward a second exit. Same headline price. Completely different movie.

The buyout structures entrepreneurs actually encounter

1. Buyout with existing management

This is the cleanest founder story. The sponsor likes the team, likes the market, and believes the company can scale with better capital, sharper governance, or a clearer value-creation plan.

2. Buyout with new management or a supplemented team

Sometimes the investor wants to keep part of the leadership bench but add a new CEO, CFO, or operating executive. That is often a signal that the sponsor sees real value in the company but believes the next stage needs a different operating cadence.

3. Platform acquisition plus add-ons

This is common in fragmented industries. The sponsor buys a strong initial platform and then uses that business to acquire smaller companies in the same space. If your company is being sold into a platform, your valuation, role, and future influence may look very different than if your company is the platform itself.

4. Club deal

When the deal is large or risk is shared across investors, multiple financial sponsors may invest together. More capital can help. More owners can also mean more complexity around control, governance, and exit timing.

Why leverage is powerful and why founders should respect it

Debt is one of the reasons buyouts can produce attractive returns for investors. If the company grows and the debt gets paid down, equity value can compound faster than it would in an all-cash acquisition. That is the upside.

The harder truth is that leverage can turn a good business into a constrained business if the company misses plan, loses a major customer, faces margin compression, or simply enters a tougher credit market. Founders should not treat debt as background noise. In many deals, debt becomes the quiet governor on what the company can do next.

That means the right diligence question is not just “Can the business support this debt today?” It is “Can the business still support this debt if the next eighteen months are merely okay instead of great?”

Rollover equity: the source of excitement and confusion

Rollover equity is where founders often shift from seller to continuing owner. Instead of taking all cash, the founder keeps some value invested in the post-closing business. This can create a real second payday if the company performs and exits well later.

But rollover equity is not magic. It is a new security in a new structure with new rules. The founder needs to understand dilution, liquidation waterfalls, governance rights, transfer restrictions, vesting or forfeiture concepts if compensation is involved, and the practical difference between owning a lot of common equity under a heavy debt stack versus owning a smaller but cleaner economics package elsewhere.

A simple example

A founder sells a company for $50 million and rolls $10 million into the new structure. If the business later doubles in enterprise value, that rollover may become the most interesting part of the original transaction. But only if the post-closing leverage, dilution, incentive pool, and preference stack leave meaningful value for that equity class on exit.

The documents founders should care about most

Lawyers will manage a large document stack. Entrepreneurs do not need to memorize every agreement, but they do need to understand where the real business terms live.

Acquisition agreement

This is where price, structure, indemnity mechanics, conditionality, termination rights, and closing risk come together.

Rollover and subscription documents

This is where your continuing equity investment is documented and where misunderstandings about economics often begin.

Equityholder or LLC agreement

This governs control, transfers, drag rights, tag rights, board rights, and the practical reality of being a minority owner after closing.

Employment and incentive documents

If you are staying, these terms shape your upside, downside, vesting, termination treatment, and alignment with the sponsor.

Debt commitment and financing documents

Even if you are not signing the credit agreement personally, the financing package can affect timing, certainty, and post-closing flexibility.

Transition services and ancillary agreements

These matter when pieces of the business need to be disentangled or supported after the deal closes.

If you are a founder, the legal issue is rarely “What does this one clause say?” The real issue is usually “How do these documents work together to shift risk, control, and economics after closing?”

Special issues entrepreneurs should not leave to the very end

Management alignment

Private equity buyers care deeply about management incentives because they are investing in a future exit, not just a present-day business. If key managers are staying, equity incentives and rollover arrangements should be designed intentionally, not stapled on after the principal deal terms are already set.

Regulatory timing

Depending on the business, industry, size of the transaction, and ownership profile, regulatory review can affect timing, cost, and even structure. This is one of the reasons sophisticated buyout timelines are often driven by more than pure business diligence.

Operational separation

When a company is being carved out of a larger business, support functions like payroll, IT, HR, and accounting can become closing-critical issues. Great deal economics can still produce a rough first year if the separation work is underbuilt.

Reverse termination risk

Founders and sellers often focus on headline consideration, but closing certainty matters too. In a debt-backed transaction, you want to understand what happens if financing wobbles, what remedies exist, and whether the seller is effectively limited to a negotiated reverse termination fee.

The founder mistakes that create regret later

- Optimizing only for valuation. The highest number is not always the best outcome if the structure is fragile or the control package is too one-sided.

- Underwriting your rollover on optimism alone. Rollover equity should be analyzed like a fresh investment, not treated as sentimental upside.

- Ignoring leverage. Debt may not sit on your personal balance sheet, but it can define the company you continue to run or invest in.

- Not clarifying your post-close role. “We’ll figure that out later” is not a strategy.

- Missing the platform versus add-on distinction. Those are different positions in the value chain and usually deserve different expectations.

- Leaving governance to summary slides. Board rights, consent rights, transfer restrictions, and drag provisions should be understood in the actual documents.

What a smart founder process looks like

A strong founder does not try to become a private equity lawyer overnight. The better move is to stay grounded in a short set of disciplined questions: What am I getting paid now? What am I rolling? Who controls the company after close? How much leverage is being added? What has to happen for my retained equity to be valuable? What happens if the financing falters? And how does my role actually change on Monday morning after the closing?

That is the difference between simply selling a company and understanding the architecture of the deal you are entering.

Strong companion topics to write next

If you want to build this into a broader founder-facing content series, these are natural follow-ons:

- Rollover equity for founders: how to think about second-bite economics without fooling yourself.

- Private equity vs. strategic buyer: when the higher offer is not the better deal.

- Management equity incentives: what executives should understand before signing the new package.

- Reverse termination fees and closing certainty: what sellers need to know in financed transactions.

- Platform versus add-on acquisitions: why the label changes the whole founder story.

- Carve-outs and transition services: why separation work often determines whether the first year is smooth or chaotic.

- Founder diligence on leverage: practical ways to evaluate whether the new capital structure is sensible.

- Going private transactions: what changes when the target is public and disclosure rules intensify.

- Representation and warranty insurance: where it helps, where it does not, and what sellers still retain.

- Club deals and sponsor syndicates: when multiple funds at the table create opportunity and when they create friction.

Use AI to pressure-test your deal

How to use the prompts below

If you want to continue analyzing a potential private equity transaction, use an AI assistant as a structured thinking tool rather than a generic explainer.

For best results, paste one of the prompts below into your preferred AI tool together with your LOI, term sheet, draft purchase agreement, rollover documents, management equity documents, employment terms, or a concise summary of the proposed transaction.

The goal is to have the AI act like a founder-side deal analysis agent that helps you understand cash at closing, rollover economics, leverage, control, incentives, closing risk, and your likely post-closing role in practical terms.

Copy-and-paste prompt for your AI assistant

Paste this prompt into your AI assistant with your deal documents or a concise transaction summary.

You are acting as a founder-side transaction analysis agent. Your job is to help an entrepreneur understand what a private equity buyout means in practical terms. Do not answer like a law professor or a generic finance explainer. Answer like a sharp deal advisor translating structure into founder consequences. Your priority is to help the entrepreneur understand: - how much value is real cash at closing - how much value depends on rollover equity, earnouts, or future upside - who controls the company after closing - how much debt is being added to the business - what risks the founder is keeping after the deal - what has to happen for retained equity to become valuable - what the founder's role, authority, and incentives will look like after closing When analyzing any buyout, assess the following: 1. Cash at closing vs. contingent value Explain what portion of the deal is guaranteed cash and what portion depends on future performance, rollover equity, incentive equity, seller notes, or earnouts. 2. Rollover equity economics Explain whether the rollover appears likely to create real upside or only theoretical upside. Consider dilution, liquidation preferences, debt load, management incentive pools, transfer restrictions, governance, and exit waterfalls. 3. Post-closing control Explain who is likely to control the board, major decisions, hiring, budgets, acquisitions, financings, and exit timing after closing. Distinguish between the founder remaining involved and the founder actually retaining decision-making power. 4. Debt and leverage Explain how the capital structure may affect the company after closing. Identify how leverage may constrain growth, hiring, acquisitions, distributions, or operational flexibility. Evaluate what happens if performance is weaker than expected. 5. Founder role after closing Explain what role the founder is likely to have after closing. Identify whether the founder is expected to remain as CEO, transition to another role, support a handoff, or leave. Flag ambiguity around authority, reporting lines, compensation, duration, and expectations. 6. Platform vs. add-on analysis Explain whether the company appears to be a platform acquisition or an add-on acquisition. Describe how that changes autonomy, integration risk, strategic importance, and future upside. 7. Management incentive analysis Explain vesting, forfeiture, repurchase rights, transfer restrictions, termination consequences, and incentive alignment in plain English. Highlight the provisions that most affect founder and executive economics. 8. Deal certainty and closing risk Identify financing risk, regulatory risk, diligence risk, consent issues, timeline risk, and any structural features that could prevent closing or change economics before closing. 9. Buyer fit Compare the practical implications of a private equity buyer, strategic buyer, or minority investor. Focus on control, culture, incentives, reporting expectations, time horizon, and likely post-closing reality. 10. Founder decision framework Help the entrepreneur answer these questions: - What am I really getting paid now? - What am I rolling, and on what terms? - Who controls the company after closing? - How much leverage is being added? - What happens if growth slows? - What is my role after closing? - What has to go right for my retained equity to be worth a lot? - Is this the right buyer for the next chapter of the business? Output instructions: For each issue, provide: 1. What it means 2. Why it matters to the founder 3. Main risks or tradeoffs 4. Questions the founder should ask 5. Red flags or common misunderstandings Style rules: - Write for an entrepreneur, not for a lawyer - Translate technical terms into practical business consequences - Focus on money, control, risk, incentives, and post-closing reality - Do not hide behind jargon - Do not assume the headline valuation tells the full story - Be direct where the structure appears one-sided or risky - If information is missing, say exactly what additional facts would matter most If documents or deal terms are provided, analyze them using this framework. If only a general scenario is provided, explain the likely founder issues, assumptions, and points requiring diligence.

Short prompt version

Use this version when you want a faster, lighter analysis.

Act as a founder-side private equity transaction advisor. Help me understand a buyout in practical terms, not just technical language. Focus on cash at closing, rollover equity, debt load, post-closing control, founder role, management incentives, platform vs. add-on status, closing risk, and what must happen for retained equity to become valuable. For each issue, explain what it means, why it matters, the main risks, the questions I should ask, and any red flags. Write for an entrepreneur and translate deal structure into consequences involving money, control, risk, and future upside.